How Do You Depreciate A New Roof On A Rental Property

How Rental Property Depreciation Works The Benefits To You

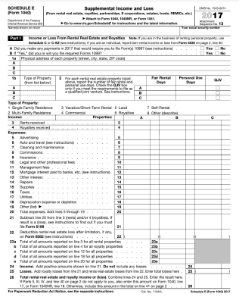

Rental Property Depreciation Rules Schedule Recapture

How To Calculate Rental Property Depreciation Morris Invest

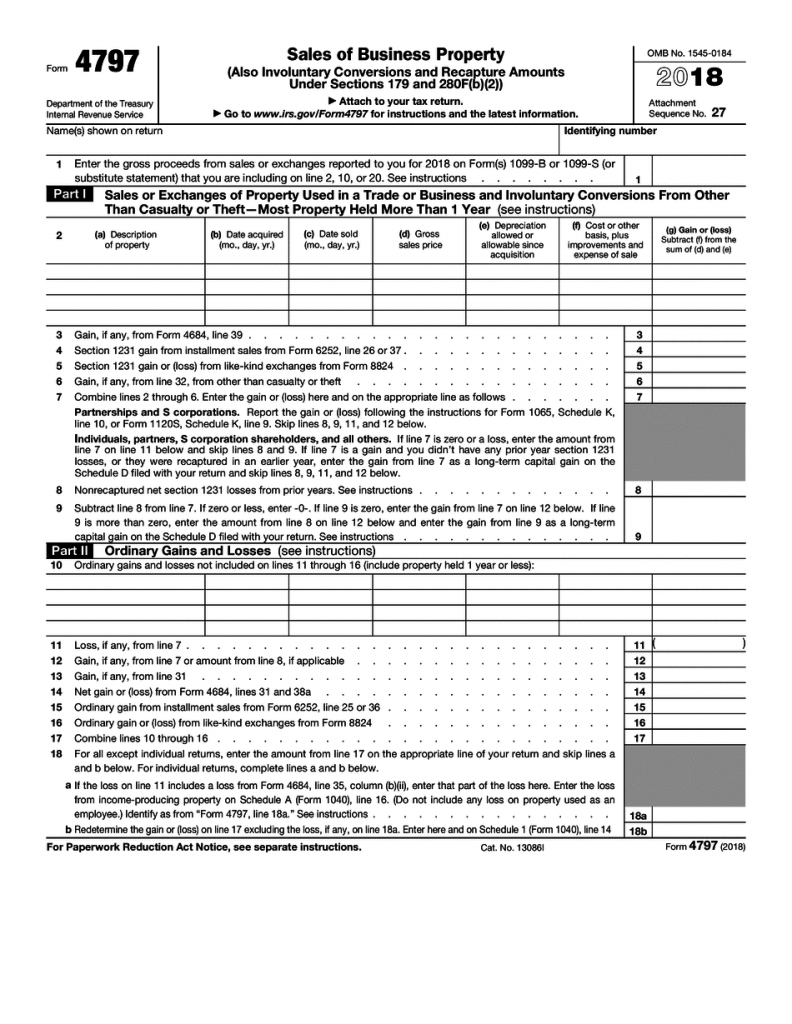

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

Understanding Depreciation Recapture Taxes On Rental Property

Rental Property Depreciation Tax Deduction Guide Wealthfit With Images Rental Property Property Rental

Depreciation starts when you bring the new roof into service.

How do you depreciate a new roof on a rental property.

Real Estate Investing Frequently Asked Questions Most Common Faqs Real Estate Rentals Renting Out Your House Rental Property

What Is Rental Property Depreciation

Video How To Maximize Rental Property Depreciation

Why Depreciation Matters For Rental Property Owners At Tax Time Stessa

Source : pinterest.com